If your heating or cooling system breaks down in the middle of summer or winter, replacing it fast becomes a top priority. However, a brand-new HVAC system can cost anywhere from $5,000 to $12,000 or more.

That is a big expense. So, can you finance an HVAC system? Absolutely — and there are more options available than most homeowners realize.

In this guide, we walk you through every way to finance an HVAC system so you can stay comfortable without breaking your budget.

What Is HVAC System Financing?

HVAC financing simply means spreading the cost of your new heating, ventilation, and air conditioning system over a period of time. Instead of paying thousands of dollars upfront, you make smaller monthly payments. Therefore, even homeowners on a tight budget can afford a quality system.

Financing an HVAC system works much like financing a car or a home appliance. You apply for credit, get approved, and then pay back the amount — usually with interest — over several months or years.

Why Should You Finance an HVAC System?

There are several strong reasons to consider financing your next HVAC installation:

- You do not have to drain your savings all at once.

- You can get a quality, energy-efficient system right away.

- Some financing plans offer 0% interest for a promotional period.

- Monthly payments are predictable and easy to budget.

- You avoid delays that could make your home uncomfortable.

In addition, a newer energy-efficient HVAC system can lower your monthly utility bills — which helps offset the cost of financing over time.

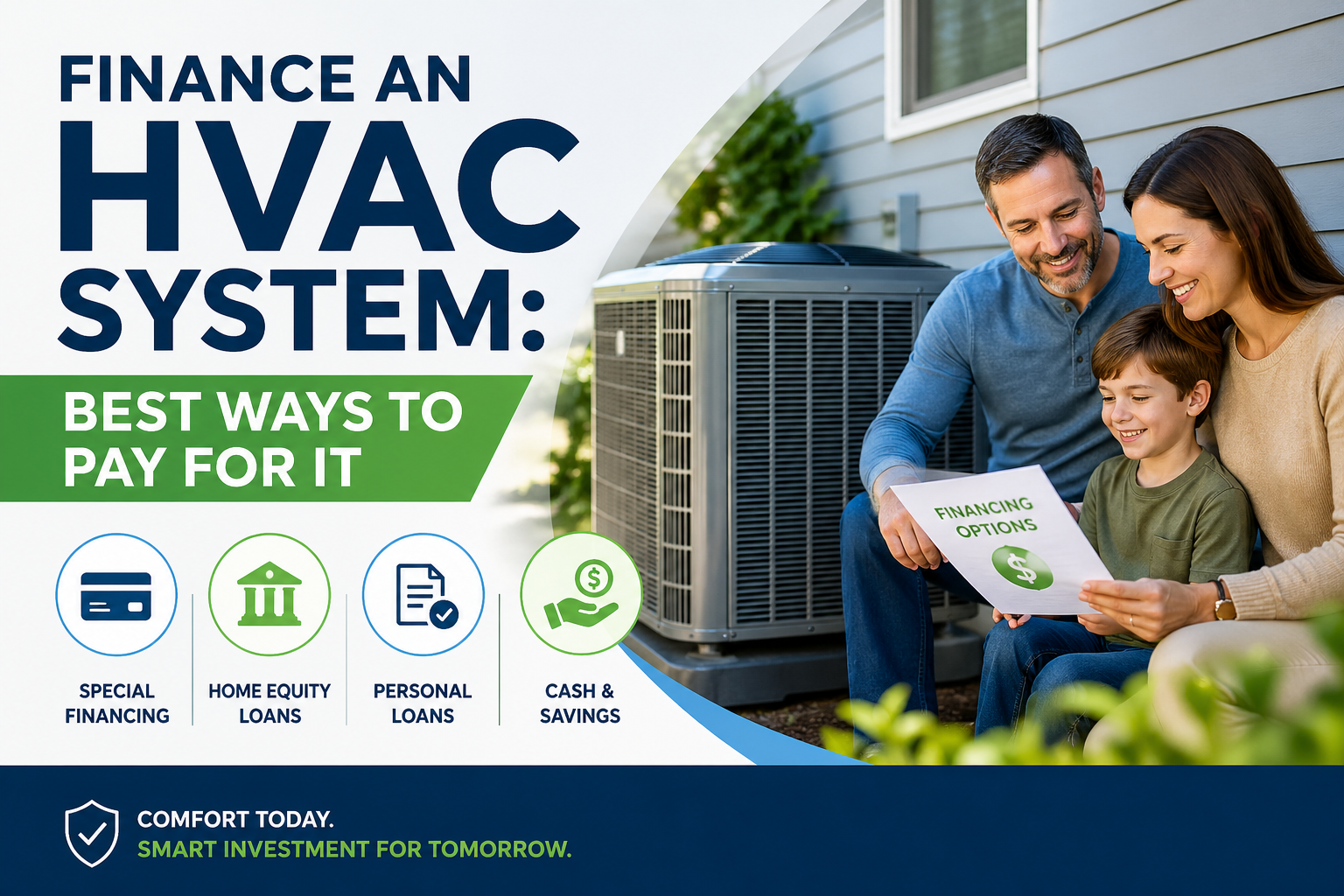

Best Ways to Finance an HVAC System

1. HVAC Manufacturer Financing

Many HVAC brands — such as Trane, Carrier, and Lennox — offer their own financing programs directly through their dealers. These programs are often the most convenient option because the dealer handles the paperwork during installation.

Some manufacturer programs come with special promotions like:

- 0% interest for 12 to 18 months

- Low fixed monthly payments

- Flexible term lengths from 24 to 60 months

However, always read the fine print. Deferred interest plans can charge you all the back-interest if you do not pay off the balance before the promotional period ends.

2. Personal Loans

A personal loan from a bank, credit union, or online lender is another excellent way to finance an HVAC system. Personal loans are unsecured — meaning you do not need to put up your home as collateral.

Key benefits of a personal loan include:

- Fixed interest rates and predictable payments

- No risk to your home equity

- Fast approval — sometimes in as little as one business day

- Loan amounts typically between $1,000 and $50,000

Therefore, if you have good credit, a personal loan can be one of the most affordable and flexible ways to finance your new system.

3. Home Equity Loan or HELOC

If you own your home and have built up equity, a home equity loan or a home equity line of credit (HELOC) can provide very low interest rates. Because your home secures the loan, lenders take on less risk and pass those savings to you.

A HELOC works like a credit card — you draw from it as needed. A home equity loan gives you a lump sum upfront. Both options are worth exploring for larger HVAC projects.

However, keep in mind that defaulting on this type of loan could put your home at risk. So only use this option if you are confident in your ability to repay.

4. HVAC Contractor Financing

Many local HVAC contractors partner with third-party lenders to offer in-house financing. You apply directly through the contractor, and the lender handles the financing in the background.

This option is convenient because:

- You can apply and get approved on the spot

- The contractor often has deals with multiple lenders

- Approval requirements can be more flexible than traditional banks

5. Government Programs and Rebates

Depending on where you live, you may qualify for government-backed programs that help finance energy-efficient HVAC upgrades. The U.S. Department of Energy, for example, supports programs that offer low-interest financing for energy-efficient home improvements.

In addition, many utility companies offer rebates when you upgrade to an ENERGY STAR-certified HVAC system. These rebates can reduce the total amount you need to finance significantly.

Learn more about energy efficiency incentives at the ENERGY STAR Rebate Finder.

6. Credit Cards

Using a credit card to finance an HVAC system is possible — but it should be your last resort. Credit card interest rates are typically high (15%–25%), which can make your system much more expensive over time.

However, if you can pay off the balance quickly or use a 0% APR introductory card, it can work in a pinch. Just be very careful about the interest charges after the promotional period ends.

How to Qualify for HVAC Financing

Qualifying for HVAC system finance options depends on a few key factors:

- Credit score — Most lenders prefer a score of 600 or higher. Better scores get better rates.

- Income — You need to show steady income to cover monthly payments.

- Debt-to-income ratio — Lenders want to see that your debts do not exceed 40%–50% of your income.

- Employment status — Being employed or self-employed with documented income helps.

Even if you have less-than-perfect credit, some HVAC contractor programs and specialty lenders still approve borrowers. Therefore, it is worth applying even if you are unsure.

How Much Does an HVAC System Cost to Finance?

The total cost of financing depends on three things: the price of the system, the interest rate, and the loan term. Here is a simple example:

- System cost: $8,000

- Interest rate: 8% APR

- Loan term: 60 months (5 years)

- Monthly payment: approximately $162

- Total interest paid: approximately $1,720

In addition, always factor in installation costs when calculating your total loan amount. A complete HVAC installation — including the unit, labor, and materials — is usually what you are financing.

For more guidance on understanding financing terms, visit Consumer Financial Protection Bureau.

Tips for Getting the Best HVAC Finance Deal

- Compare at least 3 financing offers before committing.

- Check your credit score first — you may qualify for better rates than you expect.

- Look for 0% promotional offers, but understand what happens after the promo ends.

- Ask your contractor about available rebates and utility incentives.

- Choose the shortest loan term you can comfortably afford to minimize interest costs.

- Read every detail of the financing agreement before signing.

Already installed your system? Read our guide on how to maintain your HVAC system year-round to protect your investment.

FAQS:

Can I finance an HVAC system with bad credit?

Yes, it is possible. While traditional banks may decline applicants with low credit scores, many HVAC contractors work with specialty lenders who accept borrowers with scores below 600. You may pay a higher interest rate, but you can still get approved and get your system installed quickly.

Is it better to finance or pay cash for an HVAC system?

Paying cash saves you interest charges and is the most cost-effective option if you have the savings. However, financing makes more sense when cash is tight, when you find a 0% interest promotion, or when the monthly savings on your energy bill offset the financing cost. Many homeowners find that financing an energy-efficient HVAC system actually saves money in the long run.

How long can you finance an HVAC system?

Most HVAC financing plans offer terms ranging from 12 months to 84 months (7 years). Shorter terms mean higher monthly payments but less total interest. Longer terms reduce your monthly payment but increase the total amount you pay over time. Choose the term that best fits your monthly budget without stretching the debt too long.

Conclusion: Finance Your HVAC System the Smart Way

A broken or inefficient HVAC system does not have to put you in a financial crisis. As this guide shows, there are many excellent ways to finance an HVAC system — from manufacturer programs and personal loans to government incentives and contractor financing.

Read More: Finance Charge Explained: Best Guide to Costs & Savings 2026

The key is to compare your options, check your credit, and choose a plan that fits your monthly budget. In addition, remember that an energy-efficient system can lower your utility bills every month — making the investment worth it.

Do not wait until your system completely fails. Start exploring your HVAC finance options today and take control of your home comfort on your own terms.

👉 Ready to get started? Contact a trusted local HVAC contractor today and ask about available financing plans!