Have you ever looked at your monthly credit card or loan statement and spotted a mysterious line that says “finance charge” — and had no idea what it meant? You are definitely not alone. Millions of borrowers overlook this cost every single month, and that oversight ends up costing them a fortune over time.

A finance charge is essentially the total price you pay for borrowing money. It goes beyond just the interest rate and covers every cost a lender can attach to your credit. Understanding it is one of the smartest financial moves you can make.

In this complete guide, we will break down exactly what a finance charge is, how it is calculated, what types exist, and — most importantly — how you can reduce or completely eliminate it from your financial life. Whether you are managing a credit card, a personal loan, or a mortgage, this guide has everything you need.

What Is a Finance Charge? A Clear Definition

A finance charge is the total cost of borrowing money from a lender or credit issuer. It is not just the interest you pay on an unpaid balance — it is a broader term that covers all fees and costs tied to using credit. In other words, the finance charge represents the full dollar amount you owe for the privilege of borrowing.

According to the Truth in Lending Act (TILA), lenders in the United States are legally required to disclose the finance charge to every borrower before the credit agreement is finalized. This law exists to protect consumers and give them a transparent view of what borrowing truly costs.

You will commonly encounter a finance charge in:

- Credit cards — charged when you carry a balance beyond the due date

- Personal loans — built into your monthly repayment schedule

- Auto loans — spread across the full loan term

- Mortgages — accumulated over 15 to 30 years of repayment

- Payday loans — often the highest finance charges relative to loan size

- Student loans — interest accrues during and after your study period

- Buy Now, Pay Later (BNPL) plans — finance charges may apply if you miss a payment

Therefore, no matter what type of credit you use, a finance charge almost certainly applies in one form or another.

How Is a Finance Charge Calculated?

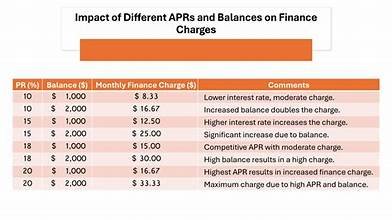

The exact calculation method depends on the type of credit product. However, the most common approach is based on your Annual Percentage Rate (APR) and the outstanding balance you carry. Here is the core formula lenders use:

| 📐 Formula: Finance Charge = Outstanding Balance × (APR ÷ 12) |

Step-by-Step Example: Credit Card Finance Charge

Let us walk through a real example to make this crystal clear:

- Your credit card balance = $2,000

- Your APR = 24%

- Monthly periodic rate = 24% ÷ 12 = 2%

- Finance charge for the month = $2,000 × 2% = $40.00

That may not sound like much. However, if you only make the minimum payment each month, that $2,000 balance could take years to pay off — and cost you hundreds of dollars in total finance charges.

Daily Periodic Rate Method

Many credit card issuers use the daily periodic rate method instead. This is calculated as:

| 📐 Formula:

Daily Rate = APR ÷ 365 | Monthly Charge = Daily Rate × Average Daily Balance × Days in Billing Cycle |

This method tends to produce slightly different results than the monthly method, so always check your cardholder agreement to know which one your issuer uses.

What Counts Inside the Finance Charge?

Beyond interest, the following items are commonly included in the total finance charge:

- Annual fees — charged each year for card ownership

- Late payment fees — added when you miss a payment deadline

- Cash advance fees — typically 3%–5% of the withdrawn amount

- Balance transfer fees — usually 3%–5% of the transferred balance

- Over-limit fees — charged when you exceed your credit limit

- Origination fees — common on personal and student loans

- Prepayment penalties — charged on some loans if you pay off early

Types of Finance Charges — Explained in Simple Terms

Not all finance charges are created equal. They fall into distinct categories, and understanding each one will help you identify exactly where your money is going.

1. Interest-Based Finance Charges

This is the most common type. Interest accrues daily or monthly on your outstanding balance, depending on your lender. The higher your APR and the larger your unpaid balance, the greater your finance charge will be. For example, a credit card with a 29.99% APR will generate a much larger finance charge than one at 14.99% for the same balance.

2. Flat-Fee Finance Charges

Some products charge a fixed dollar amount regardless of your balance. A $99 annual credit card fee, for instance, is a flat-fee finance charge. Payday loans also commonly use flat fees — for example, $15 for every $100 borrowed. These fees can be deceptively expensive when expressed as an APR.

3. Percentage-Based Transaction Fees

These charges are calculated as a percentage of a specific transaction amount. Common examples include:

- Balance transfer fee: 3%–5% of the transferred amount

- Cash advance fee: 3%–5% of the amount withdrawn

- Foreign transaction fee: 1%–3% on international purchases

4. Penalty Finance Charges

These are triggered when you violate the terms of your credit agreement. Late payment fees and returned payment fees fall into this category. In addition, some credit cards will raise your APR to a penalty rate — sometimes exceeding 29.99% — if you miss a payment. This dramatically increases your ongoing finance charge.

5. Compound Finance Charges

When interest is charged on top of previously unpaid interest, it creates a compounding effect. This is why carrying a credit card balance for a long time can result in a finance charge that far exceeds your original spending. Therefore, compounding is one of the most powerful — and dangerous — financial forces for borrowers.

Finance Charge vs. Interest Rate — Know the Difference

Many people confuse the interest rate with the finance charge. However, they are very different things. Here is a side-by-side comparison to clear it up:

Aspect |

Interest Rate |

Finance Charge |

|

Definition |

The % rate lender charges | Total cost of borrowing |

| Includes Fees? | No |

Yes — fees + interest |

|

Scope |

Narrow | Broad and complete |

| Best used for | Quick comparison |

True cost calculation |

In short: the interest rate tells you the cost of borrowing as a percentage. The finance charge tells you the actual dollar amount you will pay — including every fee your lender charges. Always look at both when evaluating any credit product.

Why Your Finance Charge Can Be Higher Than You Expect

Many borrowers are surprised when their finance charge is higher than they calculated based on the interest rate alone. Here are the most common reasons this happens:

Carrying a Balance After the Grace Period

Most credit cards offer a grace period — typically 21 to 25 days — during which you can pay your balance without incurring a finance charge. However, if you do not pay in full by the due date, interest starts accruing from the moment each purchase was made, not from the due date. This is called retroactive interest, and it can be shocking.

Making Only Minimum Payments

Minimum payments are deliberately set low to maximize the time you stay in debt. Even a $5,000 credit card balance at 20% APR, paid at the minimum payment rate, could take over 15 years to clear — with a total finance charge of thousands of dollars above the original balance.

Penalty APR Triggers

If you miss even one payment, your lender may apply a penalty APR — sometimes as high as 29.99% or more. This can cause your finance charge to spike dramatically on your very next statement.

Multiple Fees in One Billing Cycle

If you take a cash advance, miss a payment, and make a balance transfer in the same month, all three associated fees will add to your finance charge simultaneously. Therefore, even a single billing cycle can get expensive fast.

10 Proven Ways to Reduce Your Finance Charge

The great news is that you have real control over your finance charge. Here are ten strategies that work:

1. Pay Your Full Balance Every Month

This is the single most effective strategy. When you pay your credit card balance in full before the due date, most issuers waive all interest. Therefore, your finance charge drops to zero on that account.

2. Always Pay More Than the Minimum

Even adding an extra $25 or $50 per month to your payment reduces your principal faster, which in turn lowers the balance on which interest is calculated. Over time, this can save hundreds of dollars in finance charges.

3. Negotiate a Lower APR

If you have a good payment history, call your credit card issuer and ask for a lower APR. Many issuers will agree, especially if you have been a loyal customer. A lower APR directly reduces your monthly finance charge.

4. Use a 0% Introductory APR Card

Many credit cards offer 0% APR for 12–21 months on purchases or balance transfers. If you have high-interest debt, transferring it to one of these cards can eliminate your finance charge during the promotional period. However, always factor in the balance transfer fee. Check out Investopedia’s guide to low-APR credit cards for current offers.

5. Avoid Cash Advances

Cash advances carry a higher APR than regular purchases and come with an upfront fee. In addition, there is no grace period on cash advances — interest starts accruing immediately. Avoid them completely unless it is an absolute emergency.

6. Set Up Auto-Pay

Late fees are a guaranteed way to increase your finance charge. Setting up automatic minimum payments ensures you never miss a due date, protecting you from late fees and penalty APR triggers.

7. Refinance High-Interest Loans

If you have a personal loan or auto loan with a high APR, look into refinancing at a lower rate. Even a 2%–3% reduction in APR can reduce your total finance charge by hundreds or thousands of dollars over the loan term.

8. Make Bi-Weekly Payments Instead of Monthly

By paying half your monthly payment every two weeks, you end up making 26 half-payments per year — the equivalent of 13 full monthly payments instead of 12. This extra payment reduces your principal faster and shrinks your finance charge.

9. Avoid Foreign Transaction Fees

If you travel internationally, use a credit card with no foreign transaction fees. These fees — typically 1%–3% — add to your finance charge on every international purchase.

10. Read the Fine Print Before Signing

Before accepting any credit product, read the full disclosure. Under the Truth in Lending Act, lenders must clearly list all finance charges. The Consumer Financial Protection Bureau (CFPB) also offers free tools to help you compare credit offers and understand your rights as a borrower.

Finance Charges on Different Types of Credit

Finance Charge on a Credit Card

On credit cards, the finance charge appears on your monthly statement when you carry a balance. It is calculated using your daily periodic rate and average daily balance. The best way to avoid it: pay in full every month.

Finance Charge on a Personal Loan

With personal loans, the finance charge is typically front-loaded — meaning more of your early payments go toward interest and fees. This is called loan amortization. However, total finance charges decrease as you pay down principal over time.

Finance Charge on a Mortgage

Mortgages carry some of the largest total finance charges in dollar terms, simply because of their size and duration. A $300,000 mortgage at 7% APR over 30 years can generate over $400,000 in total finance charges — more than the original loan amount itself. Therefore, even small reductions in your mortgage rate can save tens of thousands of dollars.

Finance Charge on a Payday Loan

Payday loans are notorious for their extreme finance charges. A $15 fee on a two-week $100 loan seems small — but that equates to an APR of nearly 400%. These products should be avoided whenever possible.

How to Read the Finance Charge on Your Statement

Most lenders display the finance charge clearly on your monthly statement. Here is what to look for:

- “Finance Charge” line: The total dollar amount charged this billing cycle

- “Interest Charged” section: Breakdown of interest by transaction type (purchases, cash advances, etc.)

- “Fees Charged” section: Itemized list of all fees applied this cycle

- “APR” disclosure: The annual rate used to calculate your interest component

In addition, your statement should include a minimum payment warning — a box that tells you how long it will take to pay off your balance if you only make the minimum payment, and the total finance charge you will pay in that scenario. Take this warning seriously. It can be eye-opening.

You can also use our free finance charge calculator → to estimate your monthly costs based on your balance and APR.

FAQS About Finance Charges

What is a finance charge on a credit card statement?

A finance charge on a credit card statement is the total dollar amount you are charged for carrying a balance. It includes interest calculated on your unpaid balance plus any applicable fees such as late fees, annual fees, or cash advance fees.

If you pay your full balance by the due date each month, most issuers will not apply a finance charge at all.

Is a finance charge the same as interest?

No, they are not the same thing — though interest is part of a finance charge. The interest rate is the percentage your lender charges on the borrowed amount.

The finance charge is the total cost of borrowing in dollar terms, which includes interest plus all other fees such as annual fees, cash advance fees, and late payment charges. Therefore, the finance charge always gives you a more complete picture of what borrowing truly costs.

How can I avoid paying a finance charge on my credit card?

The most reliable way to avoid a finance charge on your credit card is to pay your full statement balance by the due date every month.

Most credit cards offer a grace period — usually 21 to 25 days — during which no interest accrues on new purchases if you paid your previous balance in full. In addition, choosing cards with no annual fee eliminates that component of the finance charge as well.

Can a finance charge be waived or refunded?

Yes, in some cases. If you have a strong payment history with your lender and this is your first or an occasional late fee, you can call customer service and politely request a one-time waiver.

Many issuers will grant it as a goodwill gesture. However, this is not guaranteed, and repeated requests are unlikely to succeed. The best strategy is to avoid finance charges altogether through on-time, full payments.

Conclusion — Take Control of Your Finance Charges

A finance charge is not just a confusing line on your bill — it is a real cost that affects your financial health every single month. The more you borrow and the longer you carry a balance, the more you pay. However, with the right knowledge and strategies, you can dramatically reduce — or completely eliminate — the finance charges in your life.

To summarize the key takeaways from this guide:

- Finance charges = total cost of borrowing (interest + fees)

- Your APR, balance, and repayment behavior all determine the size of your finance charge

- Paying in full every month is the most powerful way to avoid finance charges

- Reading disclosures and comparing offers helps you choose lower-cost credit products

- Small changes — like paying bi-weekly or avoiding cash advances — add up to significant savings

In addition, always remember that you have rights as a borrower. Lenders must disclose finance charges transparently under the law. Use that information to your advantage — compare, negotiate, and make smart decisions that keep more money in your pocket.

Knowledge is your most powerful financial tool. Now go use it.

💡 Start Saving on Finance Charges Today!

Now that you know exactly what a finance charge is and how it works, you have the knowledge to take action. Review your credit card and loan statements this week. Calculate what you are paying. Then use the strategies in this guide to cut those costs down — or eliminate them completely.

Every dollar saved on borrowing costs is a dollar working for your future.